Empowering Society to Pursue Sufficiency

Empowering Society to Pursue Sufficiency

The Untaken Safer Path to Climate Security and Endgame Sustainability

This is important, so I want to take some time, and step through it rather slowly.

In an opinion piece published in Scientific American on June 20, 2021, co-authors Chirag Dhara and Vandana Singh make this statement:

The key point is that efficiency is limited by physics, but there is no sufficiency limit on the socioeconomic construct of “demand.”

The Delusion of Infinite Economic Growth

https://www.scientificamerican.com/article/the-delusion-of-infinite-economic-growth/

I will accept the co-authors statement that “efficiency is limited by physics” without challenge, because I am not a physicist, so I will defer to those who are.

I am less willing to accept, without challenge, the opinion of physicists when they state “there is no sufficiency limit on the socioeconomic construct of ‘demand’”, because I do consider myself something of an expert on socioeconomic constructs, including the construct of “demand”, and my expertise tells me this is just not true.

It is true that we have to dig deep to find the sufficiency limits at work in our economy and society. It’s kind of like an archeological dig into the social structures of social decision making through which Modern Society decides what our future history can, should and will be made to be.

My claim to expertise in leading this “dig” is based on this core insight, gleaned over more that 30 years “working in the field” (not studying in Ivory Towers, where no one ever talks abu): there is a sufficiency limit on demand for investment returns by the social construct of the actuarial risk pool for programmatically providing defined benefit pension income in retirement to an evergreen, ever-changing open class of people who are retired and people who someday will be retired. This sufficiency limit is being overridden, however, by an obsolete interpretation of the fiduciary duty of pension and endowment fiduciaries that became popular during the 1970s, and needs to be upgraded today.

Once we make that upgrade, we will re-activate the sufficiency limits in our society.

The path to that upgrade begins with consideration of some specialized terms of art.

What do I mean by an actuarial risk pool?

An actuarial risk pool is a social construct that uses the Law of Large Numbers, the Mathematics of Probabilities and the Science of Statistics to average the costs of future financial uncertainities across a statistically significant population of statistically similar individuals to programmatically provide certainty against those uncertainties.

One example of an actuarial risk pool is life insurance, which uses actuarial risk pooling to programmatically provide certainty against the financial uncertainties of dying too soon. Another example is a defined benefit pension plan, which uses actuarial risk pooling to programmatically provide certainty against the financial uncertainties of living too long.

What do I mean by defined benefit pension income?

A defined benefit pension plan differs from a defined contribution savings plan in this way:

a pension plan uses actuarial risk pooling;

a savings plan does not.

If you participate in a defined benefit pension plan, you will never find yourself living without any money to live on (as long as the plan itself does not fail).

If you participate only in a defined contribution savings plan, you could find yourself living without any money to live on, depending on a number of factors, including: how much you were able to save for your retirement while you were earning money; how much you spend from your savings while living in retirement; how many investment losses you incur investing your savings; and how long your retirement lasts.

There is this simple truth about modern life: it costs money to live. Putting to one side the special case of people who inherit wealth from others (a huge conversation in its own right), we all have to earn in order to spend. In order to earn, we first have to learn. If we are prosperous enough, personally, to earn more than we need to spend on everyday living, we can save these surpluses to spend later (such as in our retirement, when we can no longer, or choose to no longer work in order to, earn). If we are prosperous enough to save sufficient sums, we can invest those savings, putting our money to work, making more money.

There are lots of reasons why people save, and a number of choices for how we can invest our savings. When it comes to savings for retirement, we have three basic choices:

we can go it alone, entirely, saving whatever amounts we choose to save, whenever we choose to save them, and investing them however we choose to invest them;

we can participate in a Defined Contribution Savings Plan (in the US, this would be 401(k) plan, or its equivalent), agreeing to have specified amounts taken out of our paycheck each pay period to be invested in one or more mutual funds or other investment programs that we choose from among a limited number of choices pre-selected by the plan sponsor (although self-directed investing can sometimes also be an option); or

we can participate in a Defined Benefit Contribution Plan (a pension plan), according to which a portion of our compensation is paid in the form of contributions to the pension plan that are owned, together with contributions made as part of the compensation package of other plan participants, by plan fiduciaries who have the legal right to invest that money any way they choose, put the fiduciary duty under the law to invest prudently, for the sole benefit of the plan beneficiaries. Which raises the important question, Who are the beneficiaries? To which the answer has to be all the people who are now or may in the future participate in the plan, who are now, or may one day become, retired.

Not everyone can choose to participate in a pension plan, because pension plans have to be offered by the places where we work, and not every place of work offers a pension plan. For those of us who do participate in a workplace provided pension plan, however, how the fiduciary owners of the money aggregated inside that plan invest that money is a matter of considerable importance to us, because every pension plan is designed, in part, on the assumption that the money aggregated inside the plan will be invested to generate a regularly recurring contribution of new money into the actuarial risk pool (while, of course, not losing any of the principal!).

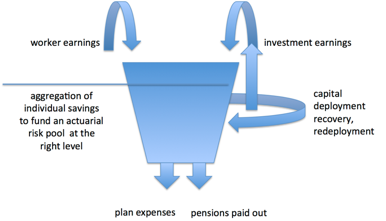

The workings of a pension pool can be visualized using a faucets-and-drains visual metaphor.

Contributions to the plan made over time as part of the compensation package for plan participants aggregate in an actuarial risk pool that is constantly being “topped up” through two “faucets” and drawn down through two “drains”.

The “faucets” consist of:

ongoing contributions as part of the total earnings package for current workers, who are also future retirees; and

cash earned on investments made by the plan fiduciaries using money in the risk pool.

The “drains” consist of:

the ordinary and necessary costs of administering the pension plan; and

current income payments to past workers who are current retirees.

The design purpose of the pension plan is to keep the “faucets” and the “drains” in proper balance, so that the pool remains properly full and prosperously flowing benefits to current retirees, in the present, and future retirees in the future, more or less forever.

And so, the fiduciary purpose of the fiduciary owners of the money aggregated in a pension plan is to generate through investment sufficient cash flows through those investments to meet the design specifications set down by the actuaries who designed the plan.

There is no term, or end date, to this purpose. It is evergreen.

What do I mean by “evergreen”?

Evergreen is a term of art I borrow from the law and legal drafting, where it is sometimes used colloquially to refer to a provision in a contract that provides for the contract to be renewed automatically, unless and until one party or the other decides to bring an end to the relationship, through some affirmative action taken.

A proper defined benefit pension plan is a contract between society and the fiduciary owners of the money entrusted to that pension plan that is evergreen, in the sense that the pension plan just keeps going, paying benefits to current retirees and accepting contributions from or on behalf of future retirees, until society takes an affirmative step to close the pension down.

What do I mean by “ever-changing”?

A pension plan is an important part of a worker’s overall compensation package. As new workers are hired, new participants are accepted into the plan. As current participants die, they leave the plan. So, the exact make-up of the population of current and future retirees participating in a pension plan is always changing.

What do I mean by “open class”?

Open class means the same thing as ever-changing, but adds a specific legal connotation under the common law of trusts, which is the primary body of law that governs the fiduciary duties of the fiduciary owners of the money that society entrusts to our various pension plans for different subsets of our population.

In the law of trusts, there are four different kinds of fiduciary duty. They are as follows.

Agent for a Principal. There is the fiduciary duty that an agent owes to their principal, a duty which is circumscribed by the terms of that agency.

Fiduciary Ownership for a Closed Class. There is the fiduciary duty that a fiduciary owner for a closed class of named or otherwise determined beneficiaries, such as the classic estate planning use of a testamentary trust for the heirs of a person on their death. The class of heirs, for example, may be indeterminate until the death of the testator. But upon death, the class is closed, and only persons who qualify as heirs on that date are eligible to benefit from that trust.

Fiduciary Ownership for an Open Class. There is the fiduciary duty that a fiduciary owner for an open class of qualified participants that changes over time, such as a pension fiduciary for the benefit of current retirees and current and future employees who will some day become retirees, or an endowment for a university or foundation for the benefit of current and future grantees.

Fiduciary Ownership of a Public Trust. There is the fiduciary duty that governmental agencies owe to the general public as stewards of public lands or other commons.

Each of these legal relationships of fiduciary duty is a social contract for some kind of sufficiency.

An agent’s duty is to deliver sufficiency to their principal, within the scope and limits of their agency.

A closed class fiduciary owner’s duty is to deliver sufficiency to the closed class of named or otherwise qualifying individual beneficiaries, within the terms of the governing deed or other document of trust.

An open class fiduciary owner’s duty is to deliver sufficiency to the open class of current and possible future beneficiaries, and to the future interests of current beneficiaries, forever, within the terms of the governing charter of trust.

A public trust fiduciary owner’s duty is to deliver sufficiency to the public, now, and forever, in accordance with the governing laws.

In each of these fiduciary relationships, the law imposes a sufficiency limit on the fiduciary exercise of discretionary authority.

Much of our economy is actually driven by these kinds of fiduciary relationships, especially those that touch most closely on humanity’s relationship with Nature.

So where does this very common notion, as in that sense correctly articulated by the co-authors of the cited Opinions piece, that there is no sufficiency limit at work in our economy, come from?

It comes from a different kind of legal relationship between individuals as savers and investment in enterprise and the economy, and a different kind of social relationship between Nature and Money.

It comes from a legal construct for investment through securitization for speculation that operates by creating standard form investment agreements with enterprises operating at scale and breaking those large-scale agreements down into smaller shares that can be bought and sold between individuals at market-clearing prices within public or private alternative markets for maintaining, or establishing, a market-clearing price.

Pubic markets are known as Exchanges. Private markets are known as Funds.

The most famous of the Exchanges, even today, is the New York Stock Exchange, which is located on Wall Street, in New York City. This whole social structure for social decision making through Finance as securitization for speculation is popularly known as Wall Street. It is also sometimes called the Capital Markets, or even the Markets. It is also sometimes called Capitalism, although the capitalist social structure for deciding what our economy can, should and will be made to be through investment in enterprise is more complicated that just the exchange-trading mechanism for financial decision making through speculation on future movements in market-clearing prices.

In fact, there are at work in our modern economy today six different social structures for social decision making through Finance, six different social structures through which our modern society decides what our future history can, should and will be made to be through investment in enterprise. Each of these different social structures can be thought of as a kind of capitalism, because they are all different ways of moving capital through our economy. All six of them could be called the six capitalisms.

These six different capitalisms, these six different social structures for social decision making through Finance through which we are choosing what the future of modern society can, should and will be made to be today, each performs the same three core functions of Finance:

each aggregates surpluses saved by individuals for a purpose;

each deploys those aggregations as investment in enterprises that fit that purpose; and

each returns a share of the new surpluses collaboratively co-created through successful investment in successful enterprises to the individuals whose surpluses they have aggregated.

Each of these different social structure can be identified by the promise that it makes to the individuals from whom it aggregates the surpluses that it invests into enterprise.

These are the following.

Family & Friends is a social structure for social decision making through Finance that aggregates surpluses saved to provide for our own and deploys those aggregations as patronage of enterprises for IMPACT, where “impact” is whatever the family and its friends decides is good for that family and its friends.

Church & Philanthropy is a social structure for social decision making through Finance that aggregates surpluses saved to provide for others and deploys those aggregations through grants made to enterprises for MISSION.

Taxing & Spending is a social structure for social decision making through Finance that aggregates surpluses saved to provide for public health, public safety and the public welfare and deploys those aggregations as subsidies for enterprises that further one or another pubic POLICY.

Banking & Lending is a social structure for social decision making through Finance that aggregates surpluses for safekeeping and deploys those aggregations as loans against PROPERTY.

Exchanges & Funds is a social structure for social decision making through Finance that aggregates surpluses saved to put money to work making more money, idiosyncratically and opportunistically, and deploys those aggregations through securitization for speculation on PROGRESS.

Pensions & Endowments is a social structure for social decision making through Finance that aggregates surpluses saved to programmatically provide certainty against certain of life’s uncertainties and deploys those aggregations through negotiated agreement for sharing in enterprise cash flows the are prioritized for SUFFICIENCY.

If we consider these choices visually, in the form of a decision tree map, we can see quite clearly what these different choices are, and begin to internalize what might be the rules for choosing among them well.

Except, we have this problem.

We have been, since the early 1970s, been directing the Fiduciary Owners of our Pensions & Endowments to hand over the money we have entrusted to their good judgment in pursuit of SUFFICIENCY to professionals expert at speculating on future movements in the market clearing prices of shares of various securities (stocks, bonds and other derivatives) in the markets for maintaining market clearing prices for those shares, shackling those fiduciaries with a false identity as Asset Owners whose purpose is to Allocate Assets to Asset Managers expert at trading Assets (i.e. stocks, bonds and other derivatives) over the Exchanges or through Funds.

In consequence, these markets that are designed to be dominated by individuals as the primary market participants, trading with their own money, for their own account, in pursuit of their own idiosyncratic and opportunistic objectives, have come instead to be dominated by institutional investors investing institutional money in pursuit of the best returns the markets will deliver. The promise of PROGRESS (a future of more that is better for more) has been replaced by a pursuit of GROWTH in market prices and transaction volumes that have no clear connection with any goal of making the world a better place.

In fact, this institutional pursuit of GROWTH is really a pursuit of consolidation of more and more control over more and more of the economy in the hands of fewer and fewer larger and larger corporate bureaucracies and the smaller and smaller number of actual human being who manipulate the law and the markets to exercise control over these bureaucracies for their own personal self-aggrandizement.

In the process we have lifted the limits of sufficiency from our fiduciary owners of these institutional funds aggregated for social purposes, which its why the co-authors are in some part correct when they tell us:

there is no sufficiency limit on the socioeconomic construct of “demand.” ibid.

Instead of collaboratively co-creating an economy of more that is better for more, we are collaboratively co-creating an economy and society characterized increasingly by:

Corporate Gigantism through Conglomeration and Monopolization;

Economic Elitism and Self-Accountability (which is no accountability);

Financial System Fragility (booms that go bust with catastrophic consequences);

Pension System Unreliability (paper wealth that evaporates when the boom goes bust);

Accelerating Externalization of Commercial Costs onto Society and Nature through worker oppression and environmental degradation;

Corporate Capture of Governmental Policy Making;

Political Divisiveness and Hostility;

Social Systems Collapse and Population Migrations;

Inaction on Climate and other challenges to keeping modern society ongoing.

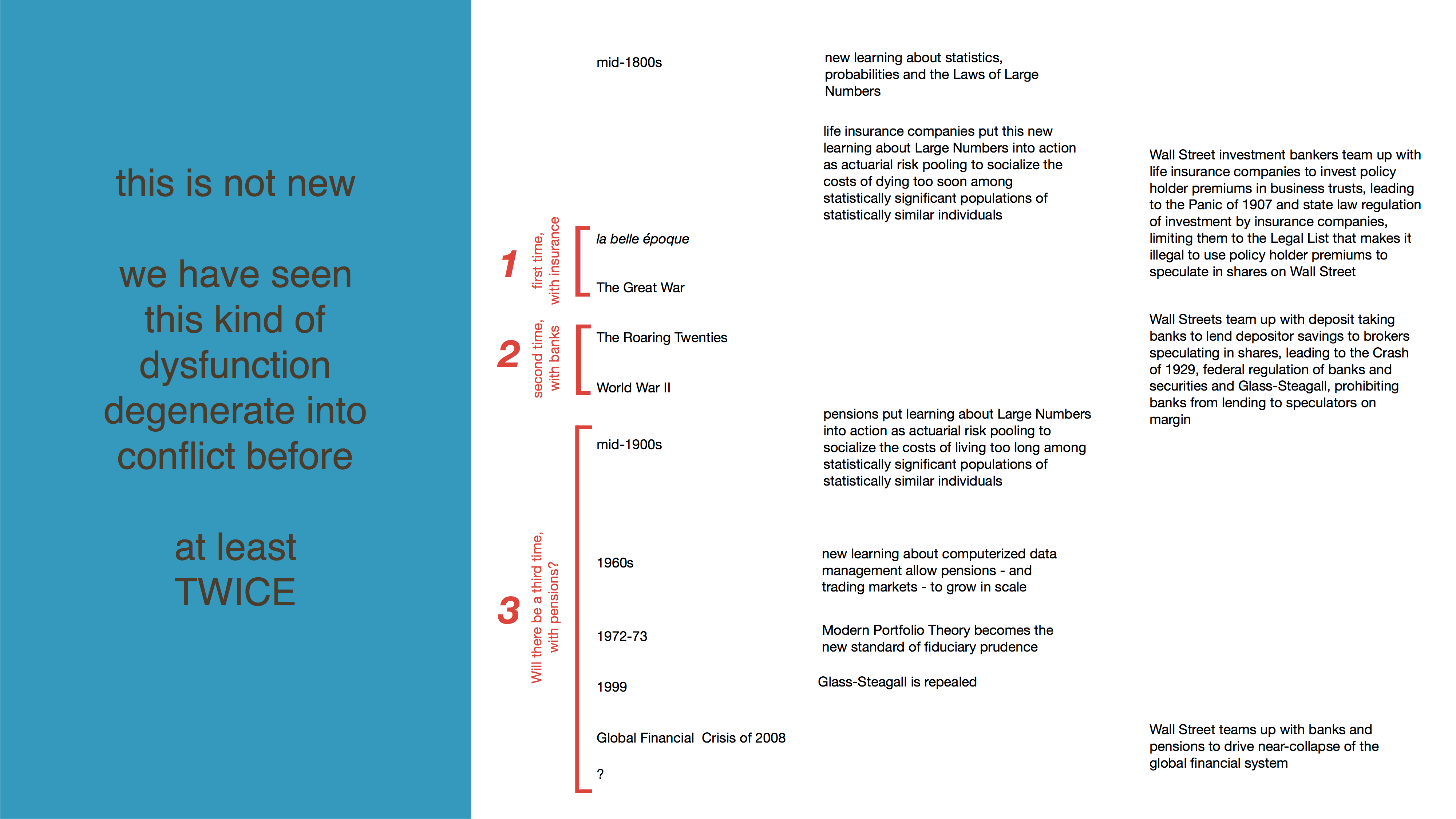

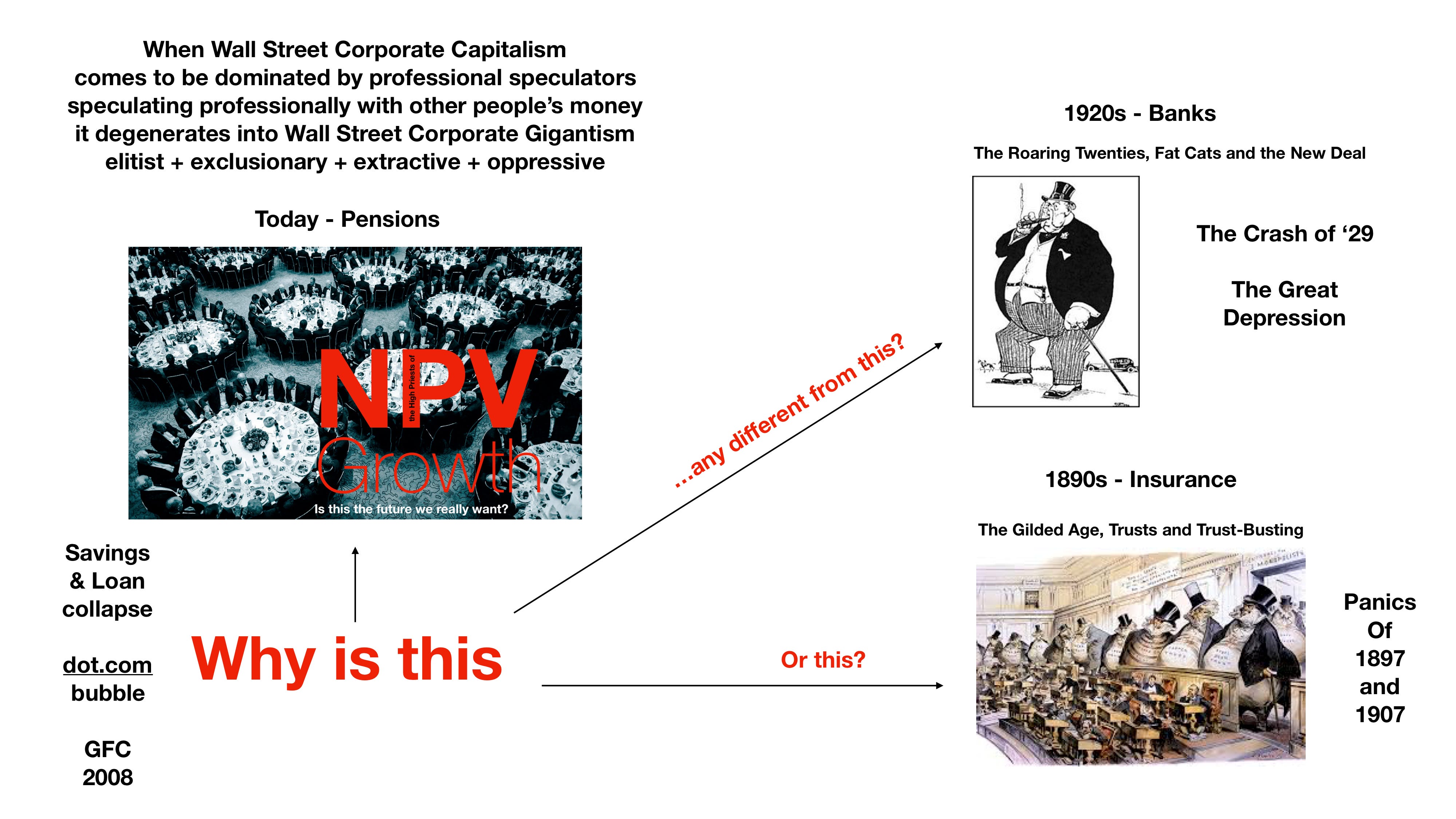

We have lived through this kind of monopolization of institutional savings by the markets for speculating in securities before. At least twice.

The first time was The Gilded Age, when life insurance premiums were misdirected into securities trading, driving a speculative asset pricing boom that went bust in the Panics of 1897 and 1907, requiring Teddy Roosevelt to ride in to bust up the trusts, while state legislatures made it illegal for insurance companies to speculate on securities with policyholders premiums.

The second time was The Roaring Twenties, when bank loans were misdirected into securities trading, driving a speculative asset pricing boom that went bust in the Crash of ‘29 and the Great Depression, requiring FDR to regulate both commercial banking and securities trading, while creating worker pensions and other social safety nets.

Today, it is happening again. This time with pensions. Why do we think it will end any differently this time, than it did in any of the earlier times?

History teaches us what we are doing wrong. Pension fiduciaries should not be speculating with pensioners money.

History teaches us the fix. Take Pension money out of Securities Speculation and put it back into Sufficiency, directly.

The question is not What? The question is How?

Bank of Nature is how.