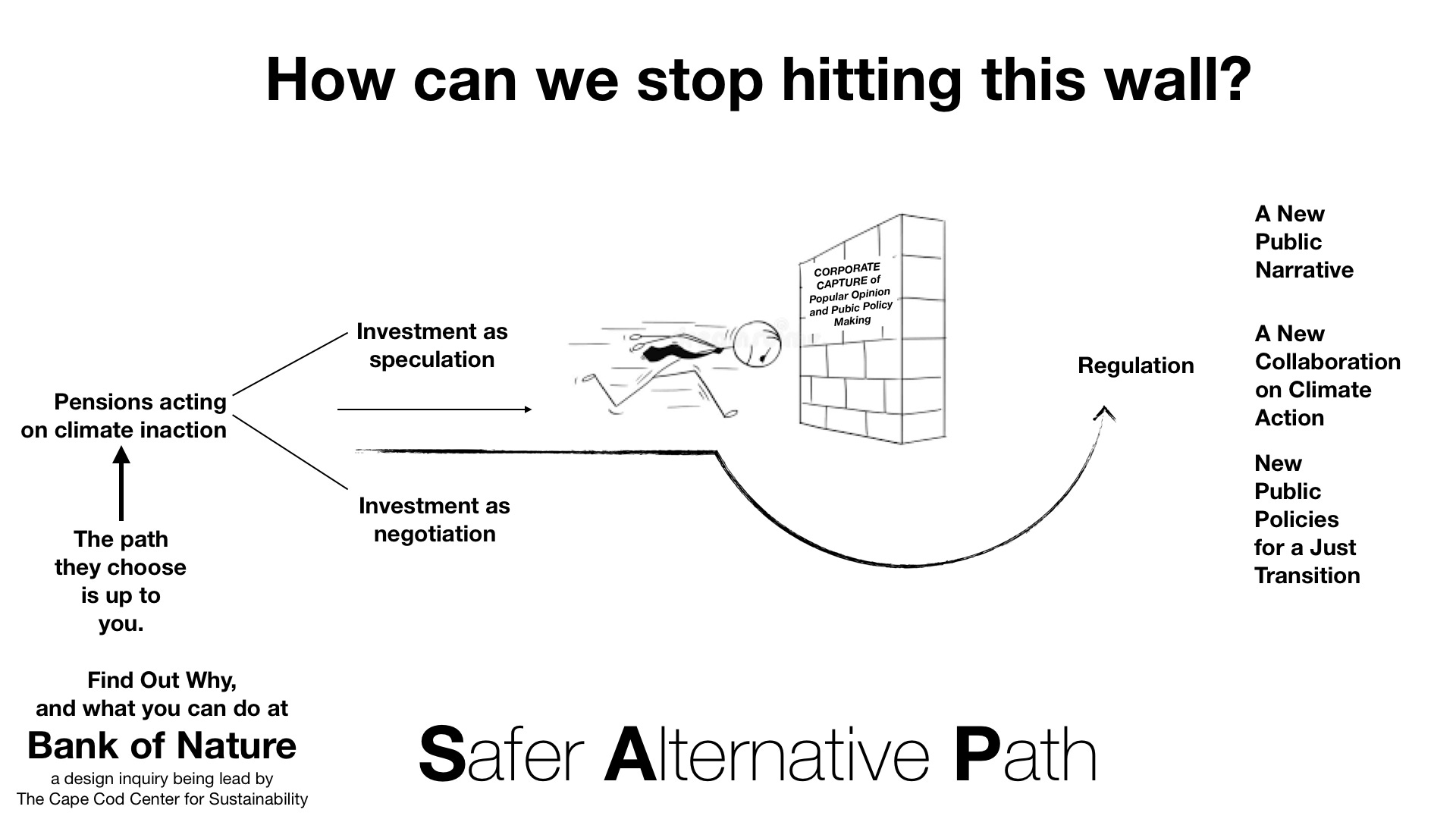

Going Around the Brick Wall of Corporate Capture

Going Around the Brick Wall of Corporate Capture

Radically Rethinking the Common Sense of Intergenerational Prudence for Pensions and Endowments as Public Trusts for Social Purposes

Adam Matthews, Chief Responsible Investment Officer for the Church of England Pensions Board and Chair of the Transition Pathway Initiative, tells us, correctly:

“All the net zero short, medium and long term commitments of pension funds we are making will hit a brick wall if there is not the enabling policy environment that drives down and reshapes demand for fossil fuels... regulation and investment have to move in tandem…”

https://www.linkedin.com/posts/adam-matthews-84926b31_climatechange-economy-sustainability-activity-6831549558040887296-vzTB

In his Week 32 post to his ESG on a Sunday Substack, entitled “We need a system change – and this is how” Sasja Beslik writes:

“3) The financial system

The main lever for change in this system is risk perception.”

Adam is right.

Sasja is not.

The main lever for change in the financial system as it is currently constituted is not “risk perception”. It is the intergenerational fiduciary duty that Pensions and Endowments owe to this generation, and the next, both equally. This is the lever that Adam Matthews can pull, to drive around the brick wall of Corporate Capture that is currently separating Investment and Regulation, making effective action on climate inaction - and other critical points of impending failure in the Human-Nature partnership that needs to be made interactive, and not extractive, right now - impossible.

In their April 20, 2021 Commentary on Corporate Law entitled Rethinking Retirement Savings, published in the Harvard Law Review Forum at 134 Harv. L.Rev. F. 348, https://harvardlawreview.org/2021/04/rethinking-retirement-savings/, Jenelle Orsi and Jason Fernandes bring us to the proper point of inquiry on this question of getting around the brick wall of Corporate Capture that is preventing pension action from driving effective climate action.

After giving us metrics on just how much money society is entrusting to these public trusts for social purposes (some $35 Trillion in the US alone), Orsi and Fernandes, writing about US retirement income laws specifically, take us directly to the Employee Retirement Security Act of 1972, as amended, popularly known as ERISA,

“which aims to provide for the economic security of American workers by requiring trustees to seek the highest risk-adjusted return on retirement plan assets”

emphasis added

This is where the law today is making a wrong turning. The authors continue,

“While this approach might be reasonable at the level of each individual pension fund, when applied at scale to the tens of trillions of dollars in U.S. retirement accounts, it is disastrous. As we demonstrate, ERISA’s strict fiduciary rules have funneled assets into the industries that have been the primary drivers of the climate crisis and rising inequality, ultimately harming the people the statute is meant to protect.”

emphasis added

The rules aren’t strict. They’re underdeveloped.

Orsi and Fernandes continue further,

“ERISA was crafted under an assumption that employees would retire into a world that is habitable and free of existential risk — an assumption that, for millennials and Generation Z, might no longer be valid. Without drastic action to avoid the effects of climate change, workers who retire toward the end of this century will inherit a world that is almost unrecognizable from our own. Roughly half of known species on Earth will face extinction. Dozens of coastal cities will be underwater. Rising sea levels, droughts, and superstorms will force hundreds of millions of people to abandon their homes in search of livable land. ERISA’s fund-maximization mandate has fueled this crisis, ensuring that American workers’ retirement savings have been subsidizing the destruction of the world they will retire into.

citations omitted

emphasis added

How did the law get us to here? The authors tell us,

Congress enacted ERISA primarily in response to a very specific problem: embezzlements, kickbacks, and “outright looting” of union-controlled pension and benefit funds. ERISA’s drafters turned to the common law of trusts, a centuries-old body of law designed to prevent such abuses. Section 403 of ERISA requires that plan assets be held in trust, and section 404 then imports duties from trust law, requiring fiduciaries to administer plans “solely in the interest of the participants and beneficiaries.”

Because of trust law’s role in ERISA’s development, courts frequently turn to trust law when interpreting ERISA. The Supreme Court has long recognized this, stating in Tibble v. Edison International that “courts often must look to the law of trusts” when “determining the contours of an ERISA fiduciary’s duty.” Trust law is therefore both the foundation of ERISA’s fiduciary responsibilities and the obvious source for resolving the statute’s ambiguities.

But the common law of trusts is ill-equipped to govern the complicated relationships between asset managers, retirement plan trustees, and millions of American workers with diverging preferences.

citations omitted

emphasis added

It is not so much that the common law of trusts is ill-equipped, as it is underdeveloped. We need to ask this unasked question, “Who are the beneficiaries?”

The duty of loyalty to beneficiaries is clear. What is less clear is who, exactly, are the beneficiaries to whom Pensions and Endowments must be unscrupulously loyal.

Let’s talk about that.

First, we have to distinguish between Pension Plans - these, in the US, include Public Employee Retirement Systems, Taft-Hartley Multi-Empower/Union Plans and Company-specific Pensions - and Retirement Savings Accounts - in the US, 401(k) plans (and their analogues) and IRAs.

Pension Plans can be thought of as Public Trusts for Social Purposes, whereas Retirement Savings Accounts are more like private trusts for individual purposes.

A private trust for individual purposes is the paradigm that most of the common law of trusts today speaks to. But unlike a proper private trust - say a testamentary trust used in estate planning - a Retirement Savings Account is not really a form of ownership so much as it is a relationship of principal to agent, where the principal is the individual who establishes an IRA or participates in a 401(k) (or equivalent), and the agent is the financial institution or employer who holds the account, and manages it exclusively for the benefit of the individual who set it up (in accordance with applicable rules of income tax law - these are, after all, creatures of the tax laws).

In these individual agency fiduciary relationships, the agent is vested with control over property belonging to the individual, and has the right to exercise the very same powers the individual could exercise for themselves, but for the tax laws.

Not so with Pension Plans as Public Trusts for Social Purposes.

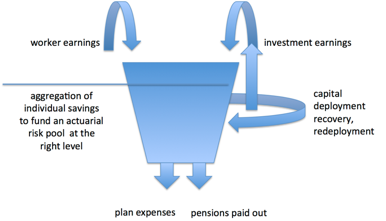

A Pension Plan is life insurance in the obverse. Where life insurance provides protection against the risk of dying too soon, pensions provide protection against the risk of living too long - and running out of money in your savings accounts!

Both are actuarial risk pools that use the Science of Statistics, the Mathematics of Probabilities and the Laws of Large Numbers to transform Aggregate Payouts into Average Costs. Participants pay in based on Average Cost, but they take out based on actual experience. If the costs are averaged correctly (by the actuaries), then Aggregate Payouts based on actual experience will equal aggregate Average Costs based on actuarial calculations.

These risk pools - actually just giant pools of money (“assets” is a slippery slope word that draws us into Corporate Capture) - are what get entrusted to Pension fiduciaries, who become fiduciary owners of all that money, with full legal right to deal with that money however they see fit. As against third parties. As against the pools sponsors and participants (workers who pay in, based on Average Cost, and are therefor entitled to take out, based on actual experience), fiduciary owners of these actuarial risk pools have a fiduciary duty to be loyal, to be prudent and to be competent.

This far, the common law of private trusts takes us, but no farther. At this point, we need to evolve a new common law for public trusts, because the fiduciary owners of these public trusts are empowered with the power of their risk pools. And no one individual participant has that much power.

What is the power that comes with fiduciary ownership of billions of dollars aggregated into an evergreen - in the sense that it is constantly ongoing, and self-regenerating - pool of money?

There are three:

size

purpose

time.

Turbo-charge these powers of size, purpose and time with the technologies of spreadsheet math and digital communication, and you get a power to negotiate custom-crafted agreements on sharing in cash flows with enterprise of any size, including the size of climate and global commerce. See, e.g. Private Equity.

With fiduciary power comes fiduciary duty constraining the use of that power.

What is the fiduciary duty of fiduciary owners of the powers of actuarial risk pools?

There is a technical answer, and a practical answer.

Technically, the duty of the fiduciary of an actuarial risk pool is to invest the money aggregated in that pool to keep that actuarial risk pool properly full, and prosperously flowing income security, with dignity, in retirement, to its retirees, today and tomorrow, across and endless series of tomorrows, pretty much forever.

Think of a pension pool as a basin outfitted with two faucets and two drains.

The “faucets” are constantly adding new money to the pool, from two sources:

average cost payments by or on behalf of current workers who will in the future become present retirees (based on average life expectancies, as calculated by the actuaries); and

statistically sufficient (as calculated by the actuaries) cash flows generated through investment of the money held in the pool.

The “drains” are constantly taking money out of the pool, for two uses:

actual costs of operating the pool, including running its investment activities; and

current income to current retirees, based on actual life experience.

The duty of the pension fiduciary is to as prudently as possible keep those faucets and drains more or less exactly balanced, so that the level of the pool remains where the actuaries have calculated it needs to be.

Practically, the duty of pension fiduciaries as investors of the money aggregated in those pools that they own is to generate statistically significant cash flows through those investments in compliance with the design assumptions made by the actuaries, today and tomorrow, forever.

Which means that pension fiduciaries have a fiduciary duty under the common law of trusts as applied to public trusts for social purposes to use their power to negotiate to generate cash flows through their investments that are sufficient for this generation of retirees, and the next, forever. That is, pensions have a fiduciary duty to the Future.

Which raises these questions of fiduciary prudence and intergeneration loyalty:

Who can and should our pension fiduciaries be negotiating with?

What can and should they be negotiating for?

This brings us back to climate action, and Corporate Capture and pension collaboration with regulation to drive real solutions to the climate crisis, and other crises of impending failure of our Human partnership with Nature, and with each other.

Pensions can negotiate with fossilized-carbon-extraction-for-combustion enterprises, directly, to finance strategies for de-commissioning their carbon activities as they replace them with new energy choices that will not increase the carbon density in our sky chemistry, thereby altering the thermodynamic balance between Earth and Space, changing long term, large scale patterns of temperature, wind, evaporation and precipitation that we call weather, in the moment, and climate over time.

Since they can, they should.

But they are not.

Why not?

To learn why not, and to find out what you can do to change their choices, ask Bank of Nature, a design inquiry of The Cape Cod Center for Sustainability.