Power That We Don’t Have

Power That We Don’t Have

As Social Institutions of Intergenerational Loyalty and Prudence Pensions & Endowments Have Powers That We, As Individuals, Do Not Have

We have this problem.

We have since the early 1970s been telling the fiduciary owners of the tens of trillions of society’s shared savings that we have entrusted to their good judgment that they can and should direct that money into our economy to help create our future prosperity through the social structures and logic for investment decision making of Corporate Finance.

We continue to do that, even today.

This is a problem because Corporate Finance is created by design for us, as individuals. Not for Pensions & Endowments as Institutions of Intergenerational Fiduciary Duty.

Corporate Finance is a social structure for social decision making through Finance that uses securitization protocols to break up large scale investment agreements into small shares that:

can be bought and sold at market clearing prices

within markets for maintaining a market clearing price

between market participants who buy and sell at the prices they choose in the quantities and at the time of their choosing

without involving the enterprise that issued those shares in order to finance its business in either the buying or the selling.

Corporate Finance is a social structure for social decision making through Finance that evolved in the 19th Century, initially as a way of raising large amounts of debt for the United States Government to finance the Civil War. It evolved out of a practice that originated in Holland in the 16th Century. There it was used to finance mercantile voyages of adventure to the Far East and other exotic locales.

It was quickly adapted to provide large amounts of equity financing to large scale industrial enterprises (think railroads, steel mills, steam ships, coal mines, newspaper printing presses, telegraph lines, gas and oil, electricity and automobiles) that were transforming the mercantile economy of the Enlightenment into the industrial juggernaut of These Our Times.

It worked initially using trusts (hence the famous trust-busting of Teddy Roosevelt) and gradually morphed into our modern practice of placing industrial scale enterprises into corporate ownership and then selling large numbers of corporate shares in small denominations to large numbers of small (relative to the total financing) individual “shareholders” who then bought and sold shares between each other, in markets for maintaining a market clearing price in those shares (“Exchanges”), without involving the corporation in any of those sales, directly.

We put the word “shareholders” in quotes because it is one of the many slippery slope words used in Corporate Finance to create in plain English an inference that is not technically correct in the language and logic of Corporate Finance.

Small shareholders technically do “own” shares in the corporations they buy shares in, but as a practical matter what they actually own is a trading position in those shares.

They can buy, hold or sell shares in whatever amounts at whatever prices at whatever times they choose, and that decision is 100% up to them. But that’s about it. Technically, they get to vote on the election of Directors, but who they get to choose from is determined largely by the incumbent executives who are running the company. They also get to vote on changes to the capital structure, such as increases in authorized shares, the creation of new classes of shares, some increases in corporate debt and some extraordinary events, like mergers, acquisitions and corporate restructurings. Of course, if there are any large voting blocks controlled, for example, by insiders, or by large institutional investors, such as Pensions or Endowments, the small votes of small investors won’t matter. Corporate elections are not like popular politics, where each citizen has one vote, and all our votes count equally with every other vote. Corporate elections are one share, one vote. Whoever owns the most shares, controls the most votes. Money rules in corporate elections. It’s not really a democracy.

Money, not The Majority, rules in corporate elections

The sale of corporate shares over the Exchanges nonetheless allowed individual savers saving in small increments to participate in the wealth being created by industrial enterprise operating increasingly at national and international scales.

It also allowed individuals to speculate manageable amounts of money in hopes of making vast fortunes by betting on new fangled technologies and technology enterprises that were changing the fabric of a rapidly industrializing global economy as they took hold and grew in popularity and wealth.

Speculating on the growth of new technologies is what Corporate Finance is created by design to finance.

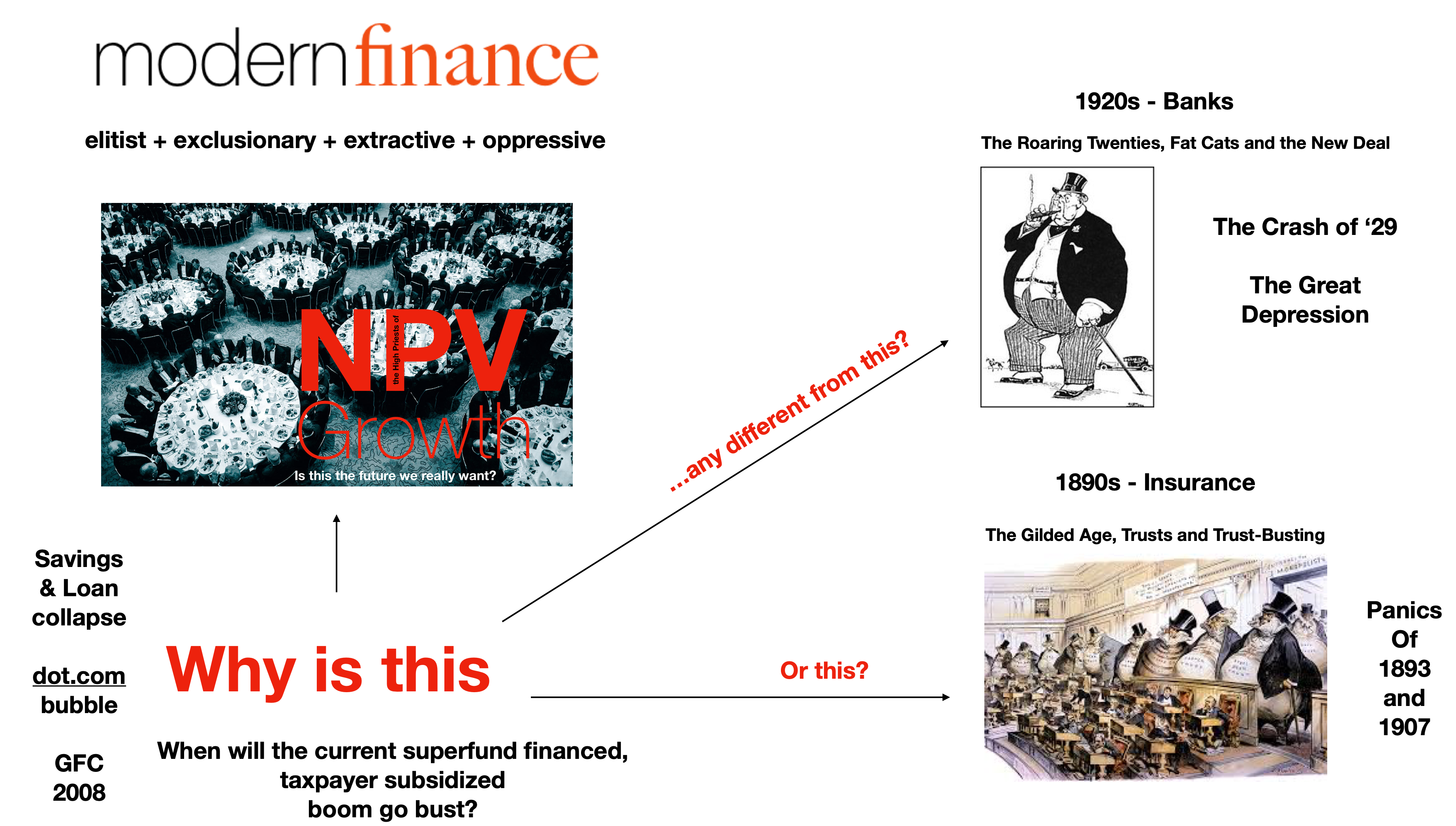

We quickly learned, however, that this structure which is designed to aggregate large sums of money in small increments from large numbers of individual buyers and sellers does not function correctly when it starts aggregating large amounts of money from small numbers of very large institutional investors that have already aggregated savings for a purpose that is not the purpose of Corporate Finance.

We first learned this lesson with life insurance companies that during the 19th Century started speculating with large amounts of policyholders premiums, fueling the stock market boom of The Gilded Age that ended in the Panics of 1893 and 1907 that almost bankrupted the US Treasury, requiring Teddy Roosevelt to ride in to bust up the trusts, while state legislatures made it illegal for insurance companies to speculate with policyholders premiums.

This lesson was not well learned, because during The Roaring Twenties depositary banks started speculating with large amounts of customer deposits, feeding another stock market boom that went bust in the Crash of ’29 and The Great Depression, requiring FDR to make laws separating commercial from investment banking and create worker pensions and social safety nets.

That lesson still did not stick. Today, pensions and endowments are speculating on stock prices - and a bewildering array of alternative so-called “financial assets” - with tens of trillions of money set aside to programmatically provide pensions in retirement for large portions of our working people, and endowment-equivalent missions.

We are living today within a stock market bubble of gargantuan proportions, fueled by pensions and turbocharged by bank deposits (Glass-Steagall, the law created after the Crash to keep banks out of Corporate Finance, being repealed in the 1990s), that almost went bust in the Global Financial Crisis of 2008, until the US Government stepped in and started just printing money in order to subsidize the stock market, which has now ballooned into what we call the global financial markets or the global capital markets. This practice of just printing money is being justified by the dubious rationale that because money today is just paper notes printed by the Government, the Government can print however many paper notes it wants to spend, without the pesky need to get voter approval for increasing taxes and more government borrowing.

So now we have a trifecta of pension money, bank deposits and the taxpayers’ credit card all supporting a stock market/capital markets booms that history and logic both teach will sooner or later go bust.

That will not be good for future us.

For present us, we are reaping what we have sown in an economy that is increasingly characterized by:

Corporate Gigantism

Economic Elitism

Corporate Capture

Political Divisiveness

Financial System Instability

Pension/Retirement System Unreliability

Social and Environmental Injustice in the Conduct of Commerce

Inaction on climate and other changes in our changing time that call for action at the scale of climate

It does not have to be this way.

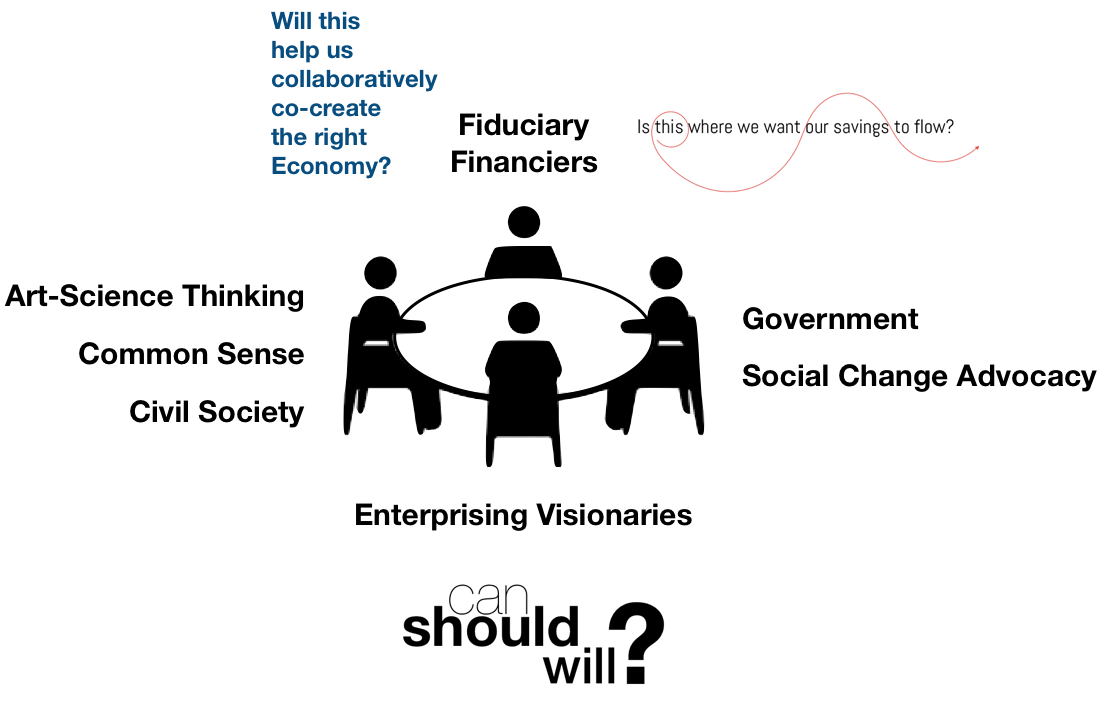

We can deflate this boom in a controlled way, before it goes bust and makes a giant mess, by moving our Pension & Endowments money out of Corporate Finance and into a new social structure of Fiduciary Finance that is created by design for institutions of intergenerational fiduciary duty.

The first step in doing that is for all of us to see that these institutions of intergenerational fiduciary duty are not “just like us”. They are, in fact, very, very different from us. They have powers that we, as individuals, do not have. They can make choices and take actions that we, as individuals, cannot. And yet we are holding them to a standard of fiduciary prudence that is the standard we would apply to ourselves.

This is not right.

We need to upgrade our standards of fiduciary prudence for these institutions of intergenerational fiduciary duty, to be fit to the power that they have, and the choices they can make.

The power that they have is the power to negotiate. The standard of prudence we hold them to must be a standard of prudence in their negotiations: Who are they negotiating with? What are they negotiating for?

The choice that they can make is that they can negotiate with any kind of enterprise of any size, and they can negotiate on formulas for sharing in enterprise cash flows that are prioritized for:

Popularity in their social contract(s) with popular choice (the source(s) of their incoming cash flows);

Sufficiency in cash flow payouts to their fiduciary financiers;

Fair Trade through their supply chains;

Accountability to Society, through compliance with the letter and the spirit of the law, good business ethics and community engagement;

Paying Nature Currently for what society takes out through that enterprise;

Fair Pay, Benefits and Working Conditions

Fair Dealing with customers and competitors in all distribution channels; and

Fair Sharing between the enterprising visionaries and their financiers (fiduciary or otherwise).

We, as individuals, of course, cannot do any of that. We do not have the size, the purpose or the time that it takes. Pensions & Endowments do. And so they can. And since they can, they should.

This is what the standards of fiduciary prudence should require them to do.

How can we make that a requirement?

By talking about it.

The law of fiduciary duty makes the common sense of commonly wise and sensible people of relevant knowledge and experience the standard of fiduciary prudence.

We are commonly wise and sensible people of knowledge and experience relevant to choosing what kind of future we want to collaboratively co-create for ourselves through the kinds of enterprises society chooses to finance.

WE can decide that it is not prudent for Pensions & Endowments to be financing enterprise value (that is, selling price) through Corporate Finance.

WE can demand that Pensions & Endowments instead direct the shared savings of society that we have entrusted, together, as society, to their good judgment into financing enterprise values (that is cash flows that are prioritized for social and environmental justice in the conduct of commerce).

We can do that by making our voices heard, over social media, in public discourse, and in petitions presented to individuals in fiduciary positions, and, if necessary, through pubic protest and demonstrations.

We can do that through social movements very much like the divestment movement. Only different in this way:

Don’t Divest. Invest.

In Decommissioning.

A Social Movement to Upgrade Standards of Fiduciary Prudence for Pensions & Endowments

The Cape Cod Center for Sustainability, through its Bank of Nature program is organizing a campaign we are calling Fiduciaries for the Future to bring Pension and Endowment fiduciaries, their professional advisors and other interested persons together in non-prescriptive, but curated, conversations for radically (in the Latin sense of “going to the root”) rethinking fiduciary duty:

PURPOSE = intergenerational reliability = future security = Common Good

POWERS = size + purpose + time + technology = negotiate = financing enterprise values (not speculating on enterprise value)

CHOICES = Who can and should you be negotiating with? What can and should you be negotiating for?

ECONOMY = our uniquely human way of being in a world of Technology that we make out of the world of Nature

ENTERPRISE = nodes in a network of exchanges for collaboratively co-creating an economy by trading surpluses

PROSPERITY = social and environmental justice in the conduct of commerce, and Society, now and in the future

FINANCE = logic systems for deciding where the money can and will be made to go

This is our Manifesto for this movement.

Fiduciaries for the Future believe:

That as fiduciary owners of pensions and endowments we have a fiduciary duty of intergenerational loyalty to the future of our current beneficiaries and also to the future of our future beneficiaries

That our populations of current and future beneficiaries are so large, and so representative of the population at large, that our fiduciary duty to their future is, de facto, a fiduciary duty to the future of everybody, not individually, but in society

That our fiduciary duty of intergenerational loyalty to the future of society requires us to “first do no harm” through our investments; that is, we are affirmatively required by our fiduciary duty NOT to make investments in the present that common sense prudence teaches can reasonably be expected to have negative adverse consequences for society in the future

That our fiduciary duty of intergenerational loyalty to the future of society affirmatively requires us to actively seek out and fund investments in the present that common sense prudence tells us can reasonably be expected to positively contribute to the possibilities for all people to live well, and with dignity, in the future

That prudently investing in the future of society is the only properly prudent way for us to constantly, consistently and reliably deliver current benefits to our current beneficiaries in the present, because today’s future is tomorrow’s present.

As large, programmatic and intergenerational fiduciary owners of society’s shared savings, Fiduciaries for the Future have the power and the technology to negotiate with enterprise of any kind and any size, directly, financing enterprise values through negotiated agreement on prioritizing cash flows for social and environmental justice in the conduct of commerce.

Fiduciaries for the Future choose to use our power as institutional intergenerational fiduciary owners of society’s shared savings to negotiate with enterprise directly on formulas for sharing in cash flows that are prioritized for social and environmental justice in the present and the future, both equally.

We are currently developing an initial website for the Bank of Nature program. This Manifesto will be posted there, with a feature that allows you to sign that Manifesto to show your support for an upgrade to our common sense of fiduciary prudence for Pensions & Endowments, from Corporate Finance to a new and better fit to purpose Fiduciary Finance.

When it is ready, please consider signing your name and making your voice be heard.